Highlights

- The performance of active largecap funds has been inconsistent. While they have outperformed in certain periods, maintaining this outperformance over the long term has proven difficult, especially in the largecap space.

- Passive investing tends to be more effective in long-term, upward-trending markets, where cost is a significant factor, particularly in the largecap space

- Considering the inconsistent performance of active largecap funds, we believe a passive strategy is better suited for largecap asset allocation.

- On the other hand, the flexicap category is most effectively managed through active strategies.

Investing in Active vs. Passive Funds Has Always Been a Topic of Debate. However, After Analyzing Historical Data, Several Key Insights Emerge:

Active flexicap managers have generally demonstrated greater reliability in outperforming their benchmarks compared to their largecap peers. The flexibility of active management in adapting to changing market conditions has consistently helped flexicap funds generate positive alpha.

Active largecap Funds have shown inconsistency in delivering excess return over their benchmarks.

As a result, a balanced approach between the two categories might be optimal. Passive strategies could be used for largecap allocation, while active managers might be used for flexicap allocation.

Fund Analysis

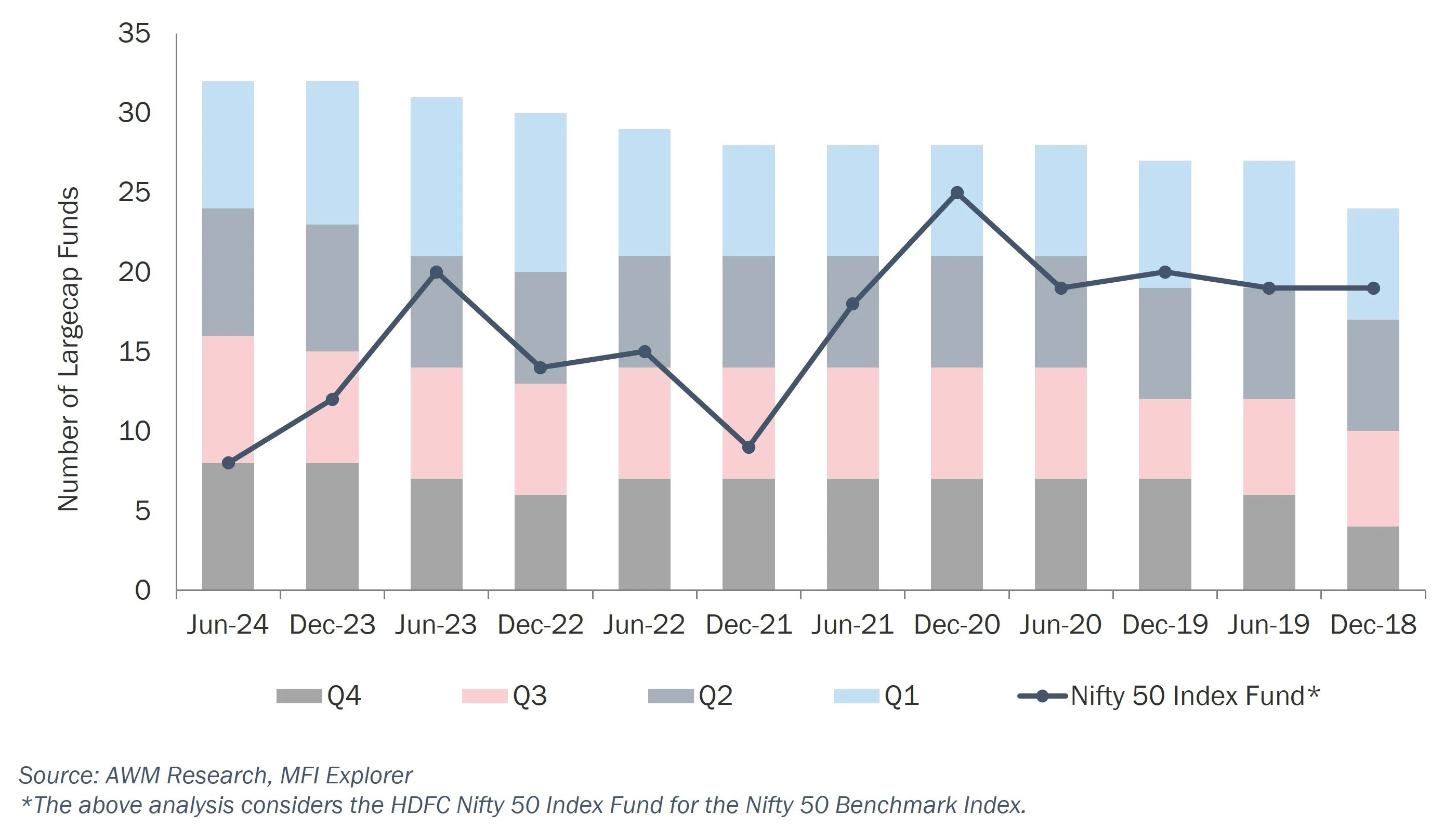

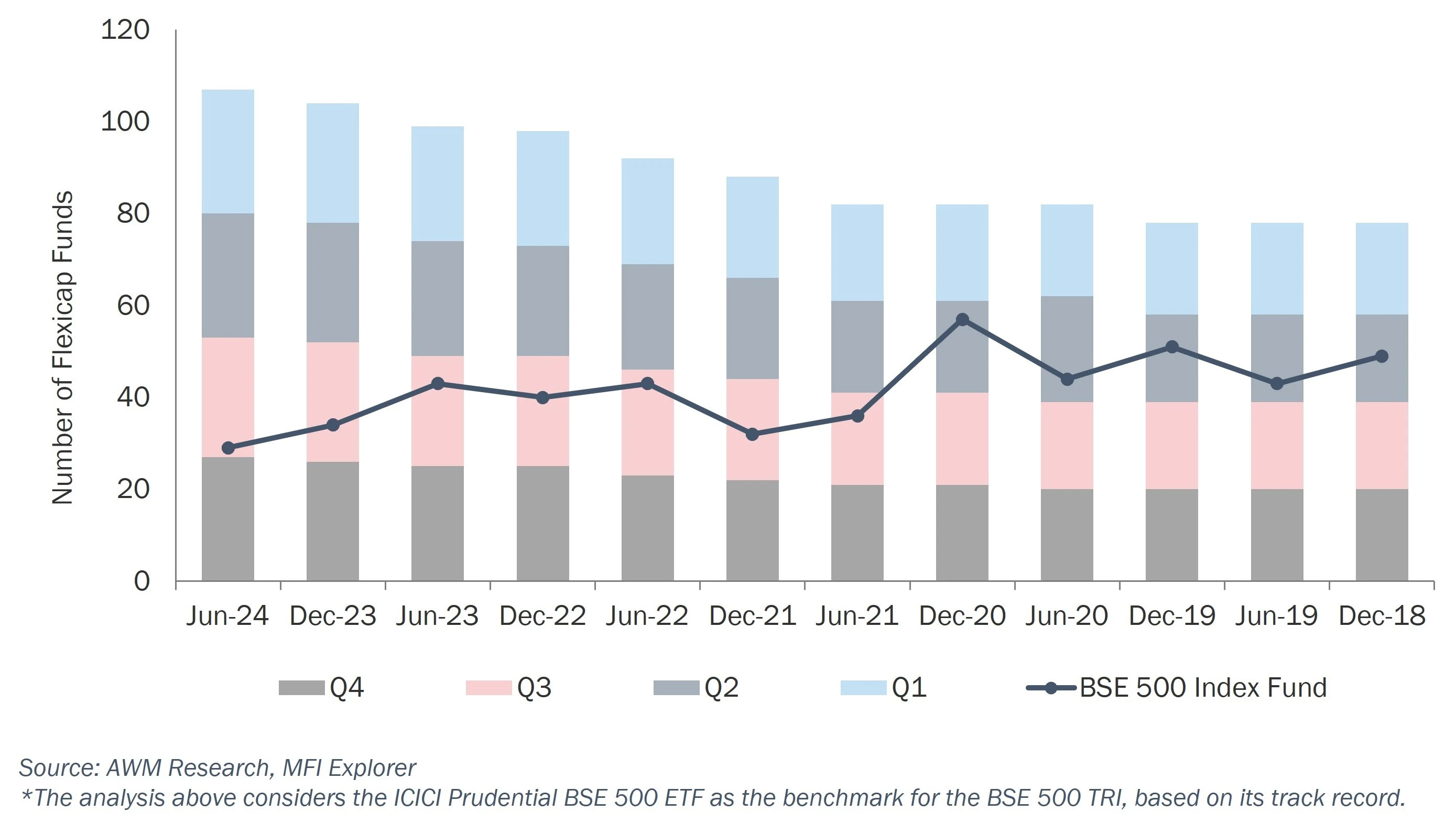

To delve deeper into these insights, we evaluated 24 to 32 active largecap funds and 78 to 107 active flexicap funds based on 3-year rolling returns, on a semi-annual basis since 2015. For the flexicap universe, we included Multicap, Flexicap, Focused, Large & Midcap, Value and Contra funds.

Large Cap Category

Active Large cap Funds 3-Year Trailing Returns

Our View

The performance of active large cap funds has been inconsistent. While they have outperformed in certain periods, maintaining this outperformance over the long term has proven difficult, especially in the large cap space. Many active funds struggle to consistently beat the market.

Passive investing tends to be more effective in long-term, upward-trending markets, where cost is a significant factor, particularly in the large cap space, where the fund's goal is to closely track the benchmark performance.

Flexi Cap Category

Active flexi cap funds have historically behaved differently to the active largecap fund category.

Out of 12 instances, the BSE 500 Index was in the third quartile (Q3) seven times on a three-year trailing basis, indicating that many flexicap active fund managers could outperform the benchmark (ICICI Prudential BSE 500 ETF).

There have been five instances where the BSE 500 Index was ranked in the second quartile (Q2).

Active Flexi cap Funds 3-Year Rolling Returns

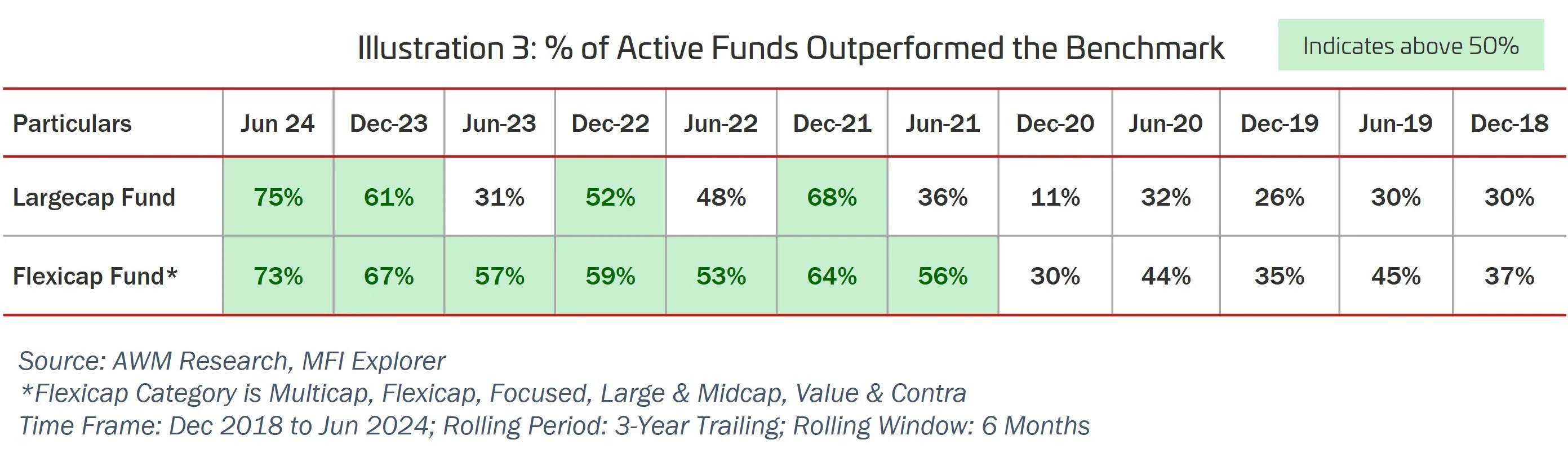

% of Active Funds that have Outperformed the Benchmark

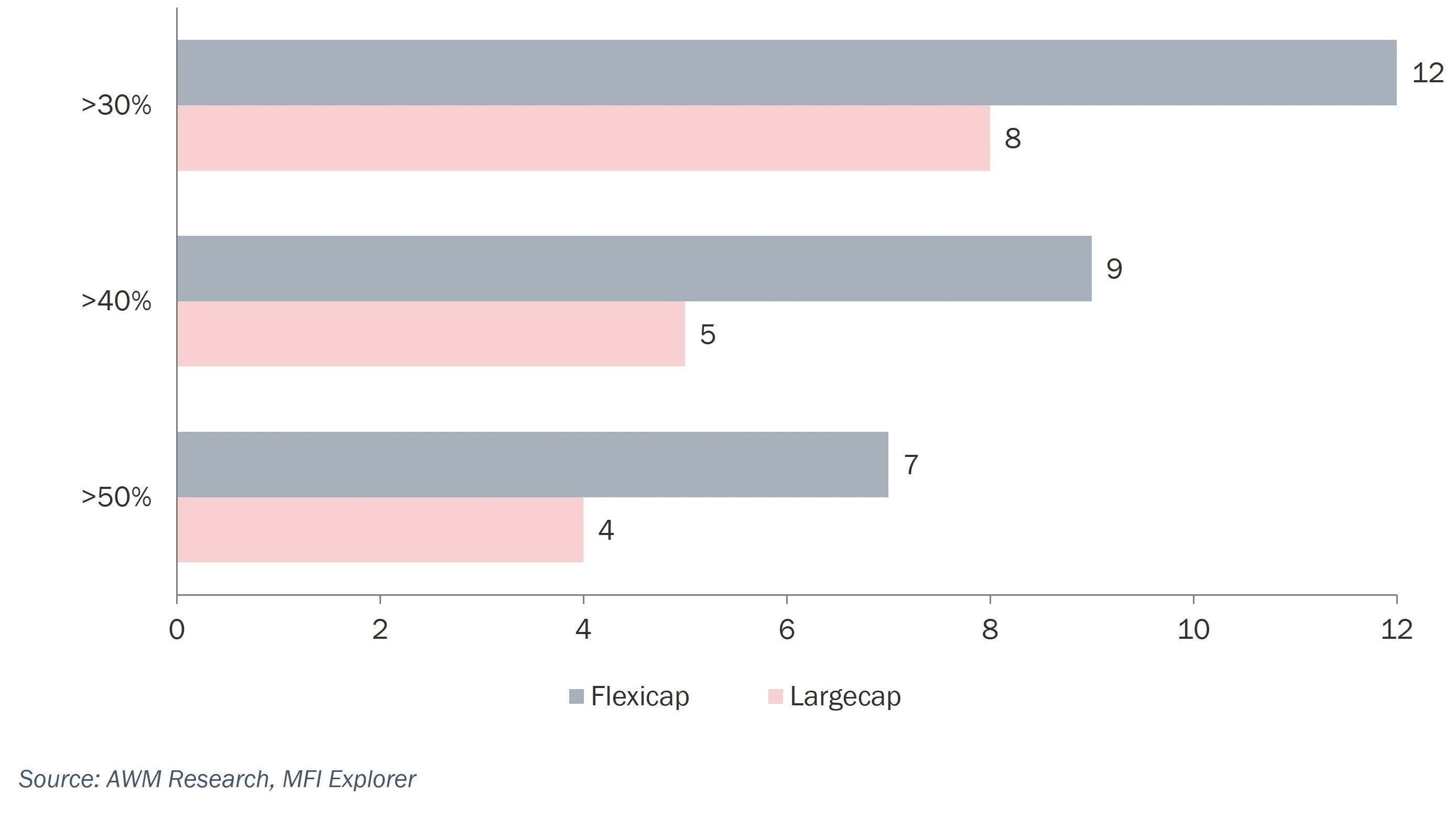

Number of Times Active Fund Have Outperformed the Benchmark

Large Cap Fund

The percentage of active largecap funds outperforming the benchmark has shown significant fluctuations over the observed periods.

The highest outperformance was seen in June 2024 (75%), while the lowest outperformance occurred in December 2020, with only 11% of funds managed to outperform the benchmark. (Illustration 3)

Recent trends indicate a recovery, with the outperformance rising to 75% in June 2024 after a low of 31% in June 2023. (Illustration 3)

Flexi Cap Fund

Active flexicap funds generally showed more consistent outperformance compared to largecap funds.

The highest outperformance was 73% in June 2024, indicating a positive recent trend. (Illustration 3)

The lowest outperformance was observed in December 2020 (30%), but there has been a steady improvement since, with the most recent figures showing 73% in June 2024. (Illustration 3)

Overall, active flexicap funds have been more resilient, with most periods showing over 50% of funds outperforming their benchmarks. (Illustration 4)

Our View

Active flexi cap funds have generally been more consistent in outperforming their benchmarks, whereas active large cap funds have struggled with consistent alpha generation.

For instance, since December 2020, over 50% of active flexi cap funds have consistently delivered alpha over their benchmark (BSE 500 TRI).

In contrast, active largecap funds have experienced uneven performance in delivering alpha over their benchmarks. Although there has been a recent recovery with noticeable improvement, the long-term trend has remained inconsistent.

Active management has proven advantageous for Flexicap Funds, where fund managers have successfully navigated across various market caps. The flexibility to adjust portfolios and adapt to changing markets has consistently helped generate alpha.

Thus, it is important to engage in a ‘Balancing Game’ between largecap and flexicap categories. Considering the inconsistent performance of active largecap funds, we believe a passive strategy is better suited for largecap asset allocation. On the other hand, the flexicap category is most effectively managed through active strategies.

Mutual fund investments are subject to market risks, read all scheme related documents carefully. For important details, please read our disclaimer.

Market Risk: Investments are subject to the standard risks associated with equity markets.

Concentration Risk: Certain funds may be concentrated consisting of a few stock ideas; may have higher volatility as well as higher drawdowns as compared to others.

Market Timing Risk: The timing of point of entry and exit in the strategy may be different in the case of certain funds which may result in a difference in performance of the funds.

Market Capitalization Risk: Certain funds may invest in securities of companies with small-to medium-sized market capitalizations which involve higher risks in some respects than investments in securities of larger companies.

Updates

Subscribe to our latest news, insights, opinions and more

Hi there!

Tell us a little about yourself and your communication preferences.